|

Risk and Assurance Committee Meeting Agenda Wednesday, 31 March 2021 9.00am Council Chamber, 28-32 Ruataniwha Street, Waipawa |

|

Risk and Assurance Committee Meeting Agenda Wednesday, 31 March 2021 9.00am Council Chamber, 28-32 Ruataniwha Street, Waipawa |

|

Risk and Assurance Committee Meeting Agenda |

31 March 2021 |

3 Declarations of Conflicts of Interest

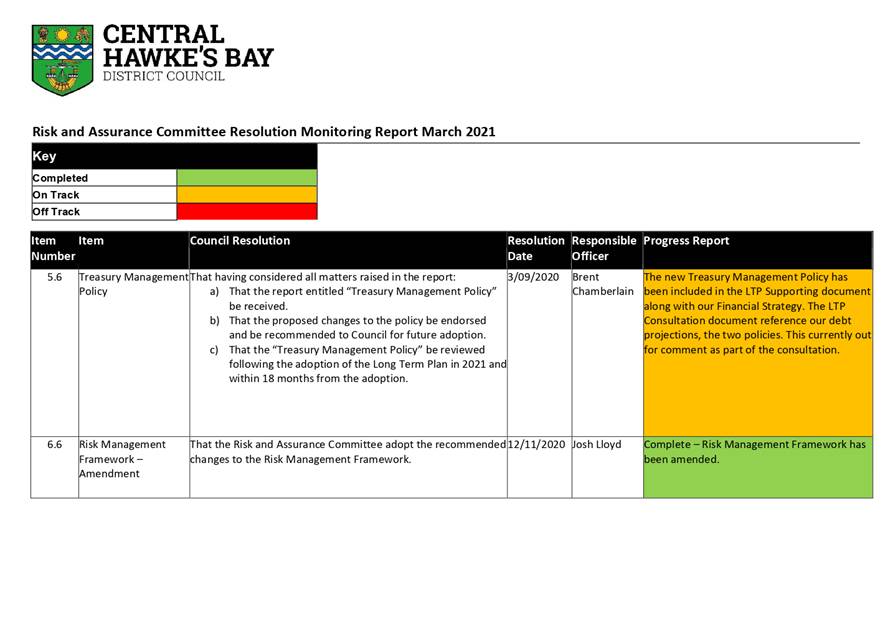

6.1 Committee Resolution Monitoring Report

6.2 Risk and Assurance Work Programme Monitoring Report

6.4 Health and Safety Update Report

6.5 Audit Findings Monitoring Report

6.6 Review of Elected Member Remuneration and Expenses Policy

6.7 Treasury Management Monitoring Report

6.8 Long Term Plan 2021-2031 Risk Mitigation

6.9 Risk and Mitigation of Earthquake Prone Council Facilities

1 Karakia

3 Declarations of Conflicts of Interest

|

RECOMMENDATION THAT the following standing orders are suspended for the duration of the meeting: · 21.2 Time limits on speakers · 21.5 Members may speak only once · 21.6 Limits on number of speakers And that Option C under section 22 General procedures for speaking and moving motions be used for the meeting. Standing orders are recommended to be suspended to enable members to engage in discussion in a free and frank manner. |

Risk and Audit Committee Meeting - 12 November 2020

|

That the minutes of the Risk and Audit Committee Meeting held on 12 November 2020 as circulated, be confirmed as true and correct.

|

|

Risk and Assurance Committee Meeting Agenda |

31 March 2021 |

MINUTES OF Central HAwkes Bay District Council

Risk and Audit Committee Meeting

HELD AT THE Council Chamber, 28-32

Ruataniwha Street, Waipawa

ON Thursday, 12 November 2020 AT

PRESENT:

Mayor Alex Walker

Cr Neil Bain (Chair)

Cr Tim Aitken

Cr Gerard Minehan

Cr Brent Muggeridge

Cr Jerry Greer

IN ATTENDANCE: Joshua Lloyd (Group Manager, Community Infrastructure and Development)

Monique Davidson (CEO)

Doug Tate (Group Manager, Customer and Community Partnerships)

Bevan Johnstone (Health & Safety Advisor)

Darren De Klerk (Director - Projects & Programmes)

Brent Chamberlain (Chief Financial Officer)

Shawn McKinley (Land Transport Manager)

1 Apologies

Nil.

2 Declarations of Conflicts of Interest

Nil.

3 Standing Orders

|

Committee Resolution Moved: Cr Gerard Minehan Seconded: Mayor Alex Walker THAT the following standing orders are suspended for the duration of the meeting: · 21.2 Time limits on speakers · 21.5 Members may speak only once · 21.6 Limits on number of speakers And that Option C under section 22 General procedures for speaking and moving motions be used for the meeting. Standing orders are recommended to be suspended to enable members to engage in discussion in a free and frank manner. Carried |

4 Confirmation of Minutes

|

Committee Resolution Moved: Cr Jerry Greer Seconded: Cr Brent Muggeridge That the minutes of the Risk and Audit Committee Meeting held on 16 September 2020 as circulated, be confirmed as true and correct. Carried |

It was requested that an amendment to the minutes were made to reflect that Councillor Aitken attended via audio-visual link.

5 Report Section

|

6.1 Risk and Assurance Work Programme Monitoring Report |

|

PURPOSE The purpose of this report is for the Risk and Assurance Committee to receive a progress update on the Risk & Assurance Committee Work Programme.

|

|

Committee Resolution Moved: Cr Tim Aitken Seconded: Cr Jerry Greer That, having considered all matters raised in the report, the report be noted. Carried |

Mrs Davidson presented the report.

It was noted that The Risk and Assurance Committee will be briefed on new Privacy Act provisions at the first Risk & Assurance Committee meeting of 2021.

Following a discussion, it was also requested that Cyber Risk, form part of a future internal audit work plan.

|

6.2 Resolution Monitoring Report |

|

PURPOSE The purpose of this report is to present to the Committee the Risk and Assurance Committee Resolution Monitoring Report. This report seeks to ensure the Committee has visibility over work that is progressing, following resolutions made by the Committee.

|

|

Committee Resolution Moved: Cr Gerard Minehan Seconded: Cr Tim Aitken That, having considered all matters raised in the report, the report be noted. Carried |

Mrs Davidson presented the report.

It was suggested that prior to Council adopt the Draft Long Term Plan 2021 – 2031, a briefing is held to the Risk and Assurance Committee on the application of the Treasury Management Policy.

|

6.3 Risk Status Update Report |

|

PURPOSE The purpose of this paper is to report to the Risk and Assurance Committee (the Committee) on Council’s risk landscape, risk management work in progress and to continue a discussion with the Committee about risk.

|

|

Committee Resolution Moved: Cr Gerard Minehan Seconded: Cr Brent Muggeridge That, having considered all matters raised in the report, the report be noted. Carried |

|

6.4 Health and Safety Update Report #4 |

|

PURPOSE To provide the Committee with health, safety and wellbeing information and insight up to the end of Q3 September 2020 and to update the Committee on key health and safety risks and initiatives.

|

|

Committee Resolution Moved: Mayor Alex Walker Seconded: Cr Jerry Greer That, having considered all matters raised in the report, the report be noted. Carried |

Officers outlined that with the implementation of the new Health and Safety system, that work continues on refining the Dashboard which was presented within the Health and Safety report. The committee requested that the report as presented, while good is very detailed and would like to see further progression towards the Dashboard report. Officers responded acknowledging that the report will continue to evolve, as the maturity of the health and safety system does.

|

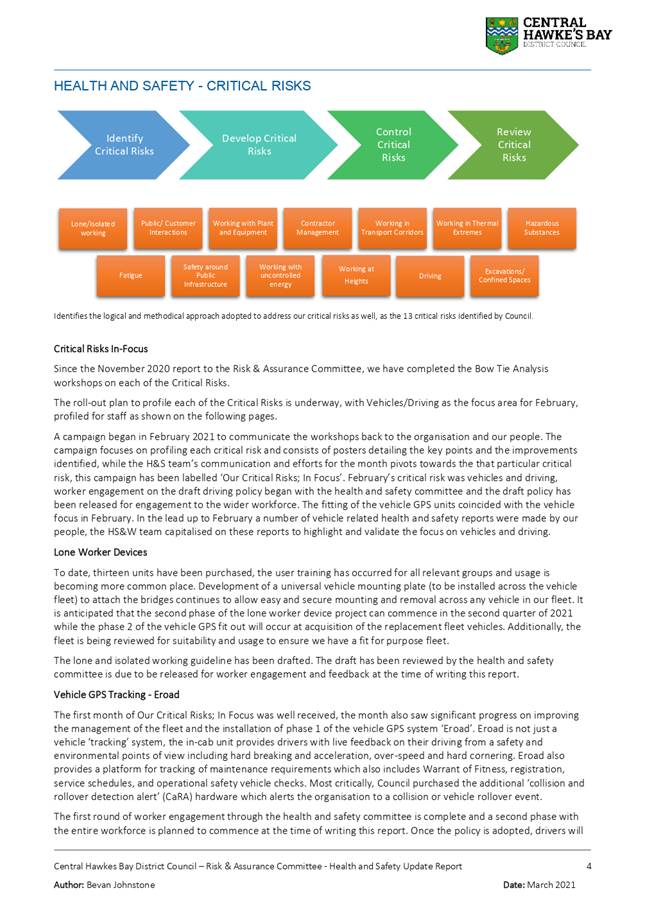

6.5 Health and Safety Critical Risks - Deep Dive |

|

PURPOSE To provide the Risk and Assurance Committee with detailed information related to the Health and Safety Critical Risks that are present in the activities Central Hawkes Bay District Council undertakes.

|

|

Committee Resolution Moved: Mayor Alex Walker Seconded: Cr Brent Muggeridge That, having considered all matters raised in the report, the report be noted. Carried |

Mr De Klerk and Mr Johnstone presented the report.

It was requested that Officers factor in the health and safety risk of Governance and executive level staff as the next step in the evolution of critical risk framework the Health and Safety space.

Health and Safety critical risks examination to be presented on an annual basis.

|

6.6 Risk Management Framework - Amendment |

|

PURPOSE The matter for consideration by the Risk and Assurance Committee is the adoption of changes to Councils Risk Framework.

|

|

Committee Resolution Moved: Mayor Alex Walker Seconded: Cr Gerard Minehan That having considered all matters raised in the report: That the Risk and Assurance Committee adopt the recommended changes to the Risk Management Framework. Carried |

Mr Lloyd presented the report.

|

6.7 Treasury Management Monitoring Report |

|

PURPOSE The purpose of this report is to provide an update on Treasury Management and Policy Compliance.

|

|

Committee Resolution Moved: Cr Gerard Minehan Seconded: Cr Tim Aitken That, having considered all matters raised in the report, the report be noted. Carried |

It was requested that forecast information on future debt funding and its origin to be included in the report going forward.

The meeting adjourned at 10:30am for a refreshment break.

The meeting resumed at 10:57am.

|

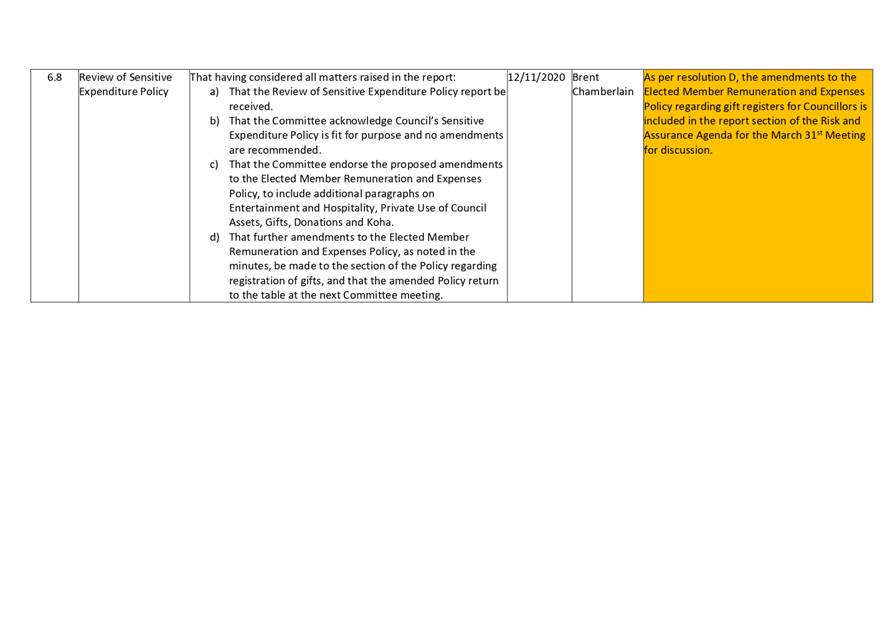

6.8 Review of Sensitive Expenditure Policy |

|

PURPOSE The matter for consideration by the Council is a review of Council’s Sensitive Expenditure Policy.

|

|

Committee Resolution Moved: Cr Tim Aitken Seconded: Cr Brent Muggeridge That having considered all matters raised in the report: a) That the Review of Sensitive Expenditure Policy report be received. b) That the Committee acknowledge Council’s Sensitive Expenditure Policy is fit for purpose and no amendments are recommended. c) That the Committee endorse the proposed amendments to the Elected Member Remuneration and Expenses Policy, to include additional paragraphs on Entertainment and Hospitality, Private Use of Council Assets, Gifts, Donations, and Koha. d) That further amendments to the Elected Member Remuneration and Expenses Policy, as noted in the minutes, be made to the section of the Policy regarding registration of gifts, and that the amended Policy return to the table at the next Committee meeting. 1. Carried |

Mr Chamberlain presented the report.

It was requested that an amendment be made to the Policy that a gift register be held. On receipt of a gift an elected member is to notify the Mayor and the Governance & Support Officer who will note the gift on the register.

That a gift value be decided upon that would trigger a gift being registered under the Policy.

|

6.9 NZTA Technical Audit 2020 |

|

PURPOSE The purpose of the report is to present the results of the 2020 NZTA Technical Audit carried out in March of 2020 inclusive of the proposed accepted corrective actions

|

|

Committee Resolution Moved: Mayor Alex Walker Seconded: Cr Gerard Minehan That, having considered all matters raised in the report, the report be noted. Carried |

Mr McKinley presented the report.

It was requested that a centralised audit report to be a standing item of the Risk and Assurance Committee.

RESOLUTION TO EXCLUDE THE PUBLIC

|

2. Committee Resolution 3. Moved: Mayor Alex Walker 4. Seconded: Cr Brent Muggeridge 5. That the public be excluded from the following parts of the proceedings of this meeting. 6. The general subject matter of each matter to be considered while the public is excluded, the reason for passing this resolution in relation to each matter, and the specific grounds under section 48 of the Local Government Official Information and Meetings Act 1987 for the passing of this resolution are as follows:

7. 8. Carried |

7 Date of Next Meeting

|

The next meeting of the Risk and Assurance Committee be held on 31 March 2021. |

8 Time of Closure

The Meeting closed at 12.20pm

The minutes of this meeting were confirmed at the Risk and Audit Committee Meeting held on .

...................................................

CHAIRPERSON

|

Risk and Assurance Committee Meeting Agenda |

31 March 2021 |

6.1 Committee Resolution Monitoring Report

File Number: COU1-1408

Author: Monique Davidson, Chief Executive

Authoriser: Monique Davidson, Chief Executive

Attachments: 1. Resolution Monitoring Report ⇩

The purpose of this report is to present to the Committee the Risk and Assurance Committee Resolution Monitoring Report. This report seeks to ensure the Committee has visibility over work that is progressing, following resolutions made by the Committee.

Recommendation

That, having considered all matters raised in the report, the report be noted.

significance and engagement

This report is provided for information purposes only and has been assessed as not significant.

DISCUSSION

The Committee Resolution Monitoring Report is attached.

Implications ASSESSMENT

This report confirms that the matter concerned has no particular implications and has been dealt with in accordance with the Local Government Act 2002. Specifically:

· Council staff have delegated authority for any decisions made;

· Council staff have identified and assessed all reasonably practicable options for addressing the matter and considered the views and preferences of any interested or affected persons (including Māori), in proportion to the significance of the matter;

· Any decisions made will help meet the current and future needs of communities for good-quality local infrastructure, local public services, and performance of regulatory functions in a way that is most cost-effective for households and businesses;

· Unless stated above, any decisions made can be addressed through current funding under the Long-Term Plan and Annual Plan;

· Any decisions made are consistent with the Council's plans and policies; and

· No decisions have been made that would alter significantly the intended level of service provision for any significant activity undertaken by or on behalf of the Council, or would transfer the ownership or control of a strategic asset to or from the Council.

|

RECOMMENDATION That, having considered all matters raised in the report, the report be noted. |

|

31 March 2021 |

6.2 Risk and Assurance Work Programme Monitoring Report

File Number: COU1- 1408

Author: Monique Davidson, Chief Executive

Authoriser: Monique Davidson, Chief Executive

Attachments: Nil

That, having considered all matters raised in the report, the report be noted.

PURPOSE

The purpose of this report is for the Risk and Assurance Committee to receive a progress update on the Risk & Assurance Committee Work Programme.

significance and engagement

This report is provided for information purposes only and has been assessed as not significant.

BACKGROUND

In 2019 following the Triennial Election, Council established a Risk and Assurance Committee, which included the appointment of an Independent Chair.

At the time that Council agreed on Council and Committee priorities, the Risk and Assurance Committee had not been fully established, therefore a formal work programme was not determined.

At the Risk and Assurance Committee meeting in late June 2020, the Chief Executive following guidance from the Independent Chair, presented a Draft Risk and Assurance Work Programme for feedback. Subsequently, The Risk and Assurance Committee Work Programme was adopted by the Committee at meeting held 3 September 2020.

DISCUSSION

The purpose of the Risk and Assurance Committee is to contribute to improving the governance, performance and accountability of the Central Hawke’s Bay District Council by:

· Ensuring that the Council has appropriate financial, health and safety, risk management and internal control systems in place.

· Seeking reasonable assurance as to the integrity and reliability of the Council’s financial and non-financial reporting.

· Providing a communications link between management, the Council and the external and internal auditors and ensuring their independence and adequacy.

· Promoting a culture of openness and continuous improvement.

The Council delegates to the Risk and Assurance Committee the following responsibilities:

· To monitor the Council’s treasury activities to ensure that it remains within policy limits. Where there are good reasons to exceed policy, that this be recommended to Council.

· To review the Council’s insurance policies on an annual basis.

· To review, in depth, the Council’s annual report and if satisfied, recommend the adoption of the annual report to Council.

· To work in conjunction with Management in order to be satisfied with the existence and quality of cost-effective health and safety management systems and the proper application of health and safety management policy and processes.

· To work in conjunction with the Chief Executive in order to be satisfied with the existence and quality of cost-effective risk management systems and the proper application of risk management policy and processes, including that they align with commitments to the public and Council strategies and plans.

· To provide a communications link between management, the Council and the external and internal auditors.

· To engage with Council’s external auditors and approve the terms and arrangements for the external audit programme.

· To engage with Council’s internal auditors and approve the terms and arrangements for the internal audit programme.

· To monitor the organisation’s response to the external and internal audit reports and the extent to which recommendations are implemented.

· To engage with the external and internal auditors on any one off assignments.

· To work in conjunction with management to ensure compliance with applicable laws, regulations standards and best practice guidelines.

· To provide a communications link between management, the Council and the external and internal auditors.

· To engage with Council’s external auditors and approve the terms and arrangements for the external audit programme.

· To engage with Council’s internal auditors and approve the terms and arrangements for the internal audit programme.

· To monitor the organisation’s response to the external and internal audit reports and the extent to which recommendations are implemented.

· To engage with the external and internal auditors on any one off assignments.

· To work in conjunction with management to ensure compliance with applicable laws, regulations standards and best practice guidelines.

Subject to any expenditure having been approved in the Long Term Plan or Annual Plan the Risk and Assurance Committee shall have delegated authority to approve:

· Risk management and internal audit programmes.

· Terms of the appointment and engagement of the audit with the external auditor.

· Additional services provided by the external auditor.

· The proposal and scope of the internal audit.

In addition, the Council delegates to the Risk and Assurance Committee the following powers and duties:

· The Risk and Assurance Committee can conduct and monitor special investigations in accordance with Council policy, including engaging expert assistance, legal advisors or external auditors, and, where appropriate, recommend action(s) to Council.

The Risk and Assurance Committee can recommend to Council:

· Adoption or non-adoption of completed financial and non-financial performance statements.

· Governance policies associated with Council’s financial, accounting, risk management, compliance and ethics programmes, and internal control functions, including the: Liability Management Policy, Treasury Policy, Sensitive Expenditure Policy, Fraud Policy, and Risk Management Policy.

· Accounting treatments, changes in generally accepted accounting practice (GAAP).

· New accounting and reporting requirements.

The Risk and Assurance Committee may not delegate any of its responsibilities, duties or powers.

The Risk and Assurance Committee is still developing, as is the maturity of the organisation in the way it manages risk and assurance matters. It is for these reasons that a 12-month work programme was adopted, with the intention in early 2021 to develop a 2-year work programme that will take Council through until the end of 2022, which also aligns with the triennial election.

The Risk and Assurance Committee will receive the following standing reports:

· Committee Priorities Monitoring Report

· Committee Resolution Monitoring Report

· Internal and External Audit Monitoring Report

· Risk Status Monitoring Report

· Health and Safety Monitoring Report

· Treasury Management Monitoring Report

The monitoring report which provides an update on the key priorities of the Committee is below:

|

Key Priority |

Responsible Officer |

Progress Update |

|

Review Internal Audit Work Programme. |

Brent Chamberlain |

On the 4th-5th March 2021 Crowe undertook a Fraud Health Check on Council, with a particular focus on its policies and internal controls. The results of this audit will be available for the May 2021 Risk and Assurance meeting. Officers were hoping to bring this to the March Risk and Assurance Committee however the report has not been completed in time.

Council has sufficient funding for generally two internal audits during each financial year. The next planned internal audit is a programme of work planned where the internal auditors will work in assisting Council to develop more comprehensive Business Continuity Plans.

Council has recently engaged an external contractor to undertake an independent Cyber Security audit. Officers are working through the draft report and intend to bring this to the May 2020 Risk and Assurance Committee meeting. |

|

Review Sensitive Expenditure Policy |

Brent Chamberlain |

This was reviewed on the 12th November 2020, but a further change was requested and the updated policy is being brought to this meeting for consideration. Assuming the Committee endorse the policy, the policy will be recommended to Council for adoption. |

|

Review Governance Policy Framework and determine role for Risk and Assurance Committee. |

Monique Davidson |

Priority will be given to this in 2021 with a planned detailed paper for the May 2021 Risk and Assurance Committee meeting. |

|

Review Risk Management Policy |

Josh Lloyd |

This is included in the Committee Agenda for November 2020. |

|

Review Risk Appetite Statement, Risk Management Policy and Governance Risk Register. |

Josh Lloyd |

Priority will be given to this in Q1 2021.

|

|

Review Fraud and Whistle Blowing Policy. |

Brent Chamberlain |

This policy will be updated once Officers receive the feedback from the recent Fraud Health Check Internal Audit.

|

|

Review Procurement Policy |

Brent Chamberlain |

The policy was last reviewed in September 2020, but Officers are in the process of updating the associated Procurement Manual to incorporate the progressive procurement toolkit and supplier guide.

|

|

Review Health, Safety and Wellbeing Governance Charter |

Darren de Klerk |

Priority will be given to this in Q2 2021 for refresh by July 2021, the Committee adopted the Charter in Q3 (July 2020).

|

|

Review Insurances and Risk Appetite |

Brent Chamberlain |

Officers, the CEO, the Chair and Deputy Chair of Risk and Assurance, and the Chair of Finance and Infrastructure, and the Mayor are scheduled to meet with AON Insurance to workshop Insurance Covers and Risk Appetite on the 30th March 2021. |

As part of the Risk and Assurance’s role in ensuring assurance on things that matter the most, regular deep dives on key issues are agreed to:

|

Topic |

Responsible Officer |

Progress Update |

|

Critical Risks |

Josh Lloyd |

Priority will be given to this in Q1 2021.

|

|

Contractor Performance |

Darren de Klerk |

Priority will be given to this in Q2 2021. Development of a a contractor management framework is close to being completed and will then be rolled out. Contractor KPIs for H&S is ongoing. |

|

Legal Challenges / Files |

Monique Davidson |

Priority will be given to this following the adoption of the Long Term Plan 2021 – 2031.

|

Implications ASSESSMENT

This report confirms that the matter concerned has no particular implications and has been dealt with in accordance with the Local Government Act 2002. Specifically:

· Council staff have delegated authority for any decisions made;

· Council staff have identified and assessed all reasonably practicable options for addressing the matter and considered the views and preferences of any interested or affected persons (including Māori), in proportion to the significance of the matter;

· Any decisions made will help meet the current and future needs of communities for good-quality local infrastructure, local public services, and performance of regulatory functions in a way that is most cost-effective for households and businesses;

· Unless stated above, any decisions made can be addressed through current funding under the Long-Term Plan and Annual Plan;

· Any decisions made are consistent with the Council's plans and policies; and

· No decisions have been made that would alter significantly the intended level of service provision for any significant activity undertaken by or on behalf of the Council, or would transfer the ownership or control of a strategic asset to or from the Council.

Next Steps

A further update will be provided at the next committee meeting 27 May 2021.

|

RECOMMENDATION That, having considered all matters raised in the report, the report be noted. |

|

31 March 2021 |

File Number:

Author: Josh Lloyd, Group Manager - Community Infrastructure and Development

Authoriser: Monique Davidson, Chief Executive

That, having considered all matters raised in the report, the report be noted.

PURPOSE

The purpose of this paper is to report to the Risk and Assurance Committee (the Committee) on Council’s risk landscape, risk management work in progress and to continue a discussion with the Committee about risk.

significance and engagement

This report is provided for information purposes only and has been assessed as not significant.

BACKGROUND

This is the fifth Risk Status Report to come to the Committee and is part of regular and routine reporting designed to provide governance with oversight and input into the way that identified risks are being managed within Council.

Further to the obvious benefits of ‘reporting up’ risk, Officers consider that these reports should be the basis of discussion that covers and adds value to all elements of the risk management spectrum (Identify, Analyse, Evaluate, Treat, Monitor/Report). That is, Officers intend that these reports facilitate discussion that identifies new risk, as well as focussing on existing listed and managed risks.

Feedback from the previous Committee meeting has shaped the structure and content of this report, with a specific focus of this report and future reports shifting to a clearer summary and assessment of risks that are considered ‘active’ at the time of reporting.

DISCUSSION

Sections below provide detail across and into Council’s risk-scape.

Risk Context and Management Approach

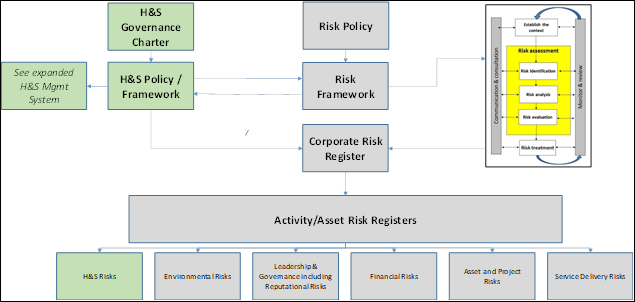

Late in 2020 the Risk and Assurance Committee (the Committee) adopted changes to Councils Risk Management Framework (the Framework). The changes to the Framework sought to ensure clarity and consistency in its application and remove ambiguity. Specifically, the risk ranking matrices were amended to align with common best practice and to be simpler.

The amended framework has been embedded in the business with existing risk registers updated to reflect the new matrix and accompanying risk descriptors. Matrix below:

Systems Development

Following the implementation of Impac Risk Manager at Council as a Health and Safety reporting system, efforts have been made to further utilise the system for the reporting on and management of all Council risks. Having all risks (corporate and safety) in a single platform allows for greater efficiency and consistency in reporting. A single system is also proven to be more helpful for users who can enter and manage risks in one place rather than many.

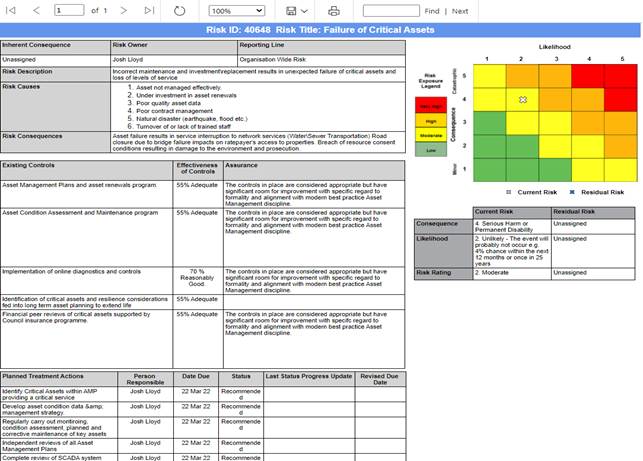

Councils highest-level strategic risks have been entered into the system and a snapshot of the reporting and management capability of this is provided below.

Example of a single risk captured in Risk Manager:

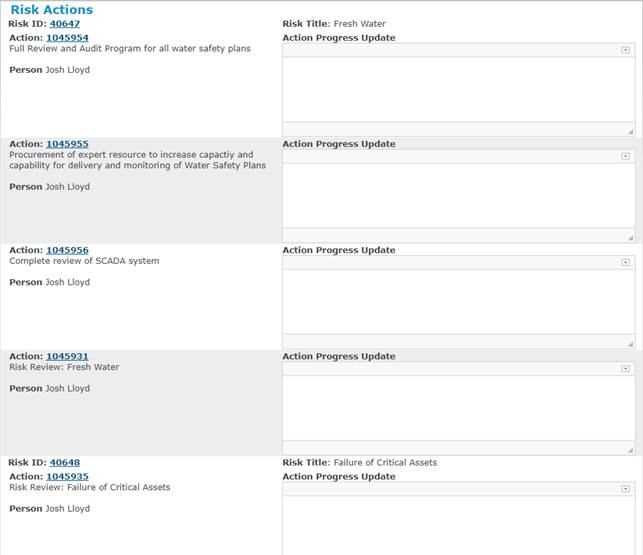

Example of Risk Actions Register with automated prompts for updates and escalation:

Example of Risk Assessment for an Individual Risk:

Now that the system has been tested and is proving valuable in managing corporate risks, the remainder of Councils existing risk registers will be transferred into the system. Namely these registers comprise operational registers for a number of activities. Customised reports are also being created to allow visibility of risk at governance, strategic and operational levels.

Health and Safety Risks

A detailed update on Health and Safety Risks is provided to the Committee in a separate report. That report covers priorities and progress and is an excellent overview of Health and Safety Risk management at Council.

Health and Safety risks to staff, contractors and the public continue to represent the highest ranking risks across all of Council activities and will accordingly remain a top priority of wider risk management approaches. Efforts continue to be made to strengthen the tie between Health and Safety risk management and corporate risk management with the implementation of a common system one of the latest advancements. Both sets of risk are now also managed by the same group within Council.

The diagram below illustrates how risk and health, safety and wellbeing integrate and overlap.

The management approach for both risk and health, safety and wellbeing are guided by strategic frameworks and policies and are influenced by National best-practice guidance material (specifically ISO-31000 and ISO-45000 series of standards).

Active Risks

In future reports it is intended that this section will be populated via an automated report run from the new Impac Risk Manager system. To enable this however, all operational risks need to be recorded in the system. This work is currently underway with the system currently housing all Health and Safety Risks as well as Corporate Strategic Risks.

The following risks are considered to be ‘active’ or ‘live’ at the time of this report, as determined by Officers. These risks span across the operational portfolios of the organisation. Some may be linked to or part of a larger Corporate Strategic Risk. This list will change from report to report as risks become live, escalate in terms of priority or are mitigated and no longer require reporting at this level.

|

Risk |

Strategic Risk Register Linkage |

Update |

|

Capital programme delivery (excl additional funding) |

Failure to effectively deliver services and projects |

The PMO is now fully established, operating and running the majority of large capital projects / programmes. Key programmes are reported on to Council including the Big Water Story, The Big Waste Water Story and PGF works. This risk remains live as there continues to be tight timeframes to deliver projects (especially those with external funding expectations) and also competition for contracting resource. Recent efforts to recommence a large capital project at the landfill have been hampered by the unavailability of the previous contractor. This remains to be managed largely on a case by case basis however is impacting the way Council design and procure its projects/programmes. |

|

Wastewater Compliance |

Wastewater treatment system failure |

The removal of floating wetlands has been completed at all facilities since the previous report. Risk through this process was managed and there were no adverse impacts on compliance. HBRC remain active and engaged in the compliance of our wastewater facilities and recently Officers have provided a formal update to HBRC to detail current compliance issues, limitations and remediation underway and planned. The relationship with HBRC remains positive and engagement is happening at both an operational and strategic level to maintain this. |

|

Condition-related asset failure |

Failure of critical assets |

Failures of 3 Waters reticulation assets continue to impact work programmes and place operational and financial pressure on Council. The LTP contains provision for significant increases in planned and reactive renewals to address pipe asset failures however until that is approved the teams and budgets remain very stretched. Contracting staff workload is of concern and is being managed with increased reporting on overtime allocations and leave balances. Efforts are being made now to source additional resource while keeping within existing financial constraints. |

|

Staff attraction / recruitment for key roles |

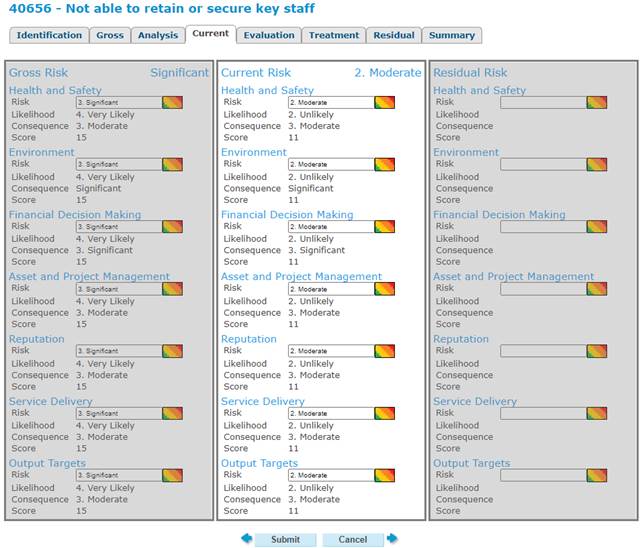

Not able to retain or secure key staff |

This has been modified from the last report to focus purely on recruitment rather than retention. This reflects current experience. Currently Council is advertising for several key roles and in some cases is on the 3rd round of recruitment trying to find suitable available candidates. In the interim this is being managed via increased engagement of external resources or through existing staff taking on extra duties for a short period. Developing a long-term people and recruitment strategy is a listed priority for the People and Business Enablement Group in 2021. |

Implications ASSESSMENT

This report confirms that the matter concerned has no particular implications and has been dealt with in accordance with the Local Government Act 2002. Specifically:

· Council staff have delegated authority for any decisions made;

· Council staff have identified and assessed all reasonably practicable options for addressing the matter and considered the views and preferences of any interested or affected persons (including Māori), in proportion to the significance of the matter;

· Any decisions made will help meet the current and future needs of communities for good-quality local infrastructure, local public services, and performance of regulatory functions in a way that is most cost-effective for households and businesses;

· Unless stated above, any decisions made can be addressed through current funding under the Long-Term Plan and Annual Plan;

· Any decisions made are consistent with the Council's plans and policies; and

· No decisions have been made that would alter significantly the intended level of service provision for any significant activity undertaken by or on behalf of the Council, or would transfer the ownership or control of a strategic asset to or from the Council.

Next Steps

Officers focus on Risk Management continues to be the establishment and embedding of a common single system for managing and reporting all risks. Significant progress has been made on this and will continue to be made over the coming weeks.

Officers welcome feedback and guidance of the Committee and its members on the future of this report and other matters with respect to Risk Management in the organisation.

|

RECOMMENDATION That, having considered all matters raised in the report, the report be noted. |

|

31 March 2021 |

6.4 Health and Safety Update Report

File Number:

Author: Nicola Bousfield, Group Manager - People & Business Enablement

Authoriser: Monique Davidson, Chief Executive

Attachments: 1. Health and Safety Update Report ⇩

<Summary Section>

That, having considered all matters raised in the report, the report be noted.

PURPOSE

To provide the Committee with health, safety and wellbeing information and insight up to the end of mid-March 2021 and to update the Committee on key health and safety critical risks and initiatives.

significance and engagement

This report is provided for information and due diligence purposes and has been assessed as not significant.

BACKGROUND

Elected members, as ‘Officers’ under the Health and Safety at Work Act 2015 (HSWA), are expected to undertake due diligence on health and safety matters.

The Health and Safety at Work Act 2015 came into law on 4th April 2016. It requires those in governance roles, and senior management, to have a greater understanding of their organisation’s health and safety activities.

Under the Health and Safety at Work Act 2015, all elected members are deemed ‘officers’ and must exercise a duty of due diligence in relation to health and safety. These quarterly reports provide information to assist elected members to carry out that role and provides the health and safety information it needs to be aware of to meet its responsibilities under the Act.

DISCUSSION

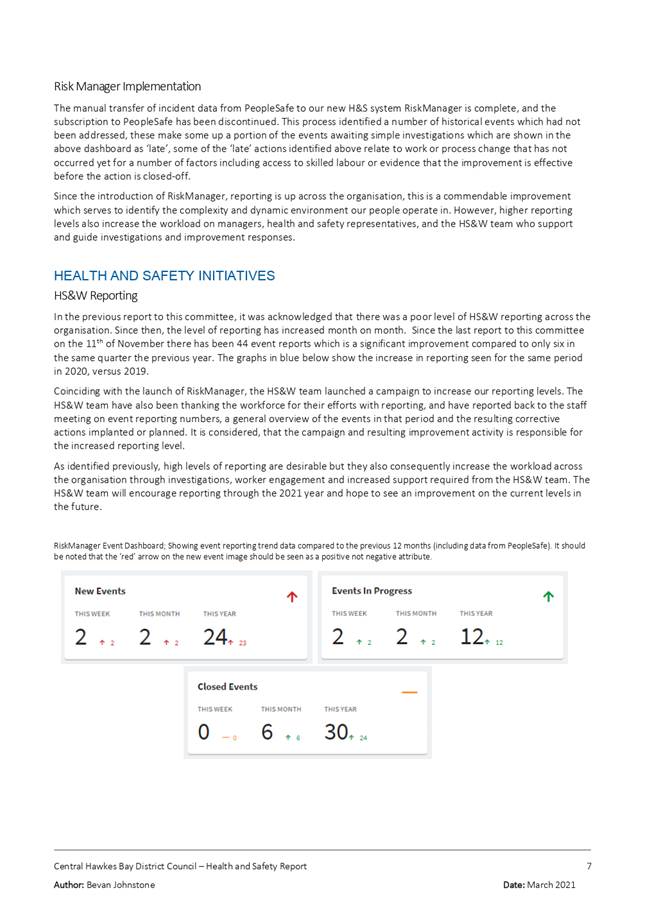

This is the update for Quarter Four of 2020 and Quarter One for 2021 – October 2020 through to March 2021. The most recent quarter has been included in the reporting period, to reduce the delay in information flow which will allow elected members a timelier overview on Health, Safety and Wellbeing (HS&W) matters and initiatives – in alignment with elected members due diligence requirements.

The HS&W team continue to work on the raft of improvements put into action in 2020, many are well underway or bedding-in, while some have required significant foundational work, or time for collaboration and worker engagement.

The new reporting system ‘Risk Manager’ has been rolled-out, implemented and is established as the single point of truth for HS&W matters in our organisation. Line managers are continuing to receive assistance and support from the H&S Advisor to manage events in the system. Reporting levels are up on previous figures; which is an encouraging sign and this has a flow on effect by the number of investigations and improvements projects. As the experience and maturity increases across the organisation, we will be better placed to manage the increased reactive workload created through increased event reporting while continuing to deliver on proactive improvements and projects identified in the Gap Analysis Project.

Since the last report; the migration of information from the old reporting system, PeopleSafe to the new system RiskManager has been completed and PeopleSafe has now been discontinued. The vehicle GPS trial has concluded and approximately half the vehicle fleet have been fitted with the GPS system ‘Eroad’. Additionally, the preferred lone worker devices were trialled by staff across the organisation, a high level of worker engagement was seen in this trial. The first delivery of lone worker devices has occurred along with training for our people in February 2021. The roll-out of the first phase of these devices has been staggered while metal mounting plates for the bridge units in vehicles has been developed.

Outside of the planned work, a district wide initiative to combat abuse and threatening behaviour directed towards stop-go sign operators at roadworks has begun.

Significant work has also gone into the policy and guideline space including; vehicle and driving, fleet management and procurement, vaccinations and isolated and lone working. As part of the lone worker device rollout, an additional internal escalation guideline has been developed to guide people leaders in the event of a genuine lone worker device activation.

As execution of these deliverables progresses, work also continues to ready for the execution of other deliverables identified in the Gap Analysis as well outcomes of event reports.

Implications ASSESSMENT

This report confirms that the matter concerned has no particular implications and has been dealt with in accordance with the Local Government Act 2002. Specifically:

· Council staff have delegated authority for any decisions made;

· Council staff have identified and assessed all reasonably practicable options for addressing the matter and considered the views and preferences of any interested or affected persons (including Māori), in proportion to the significance of the matter;

· Any decisions made will help meet the current and future needs of communities for good-quality local infrastructure, local public services, and performance of regulatory functions in a way that is most cost-effective for households and businesses;

· Unless stated above, any decisions made can be addressed through current funding under the Long-Term Plan and Annual Plan;

· Any decisions made are consistent with the Council's plans and policies; and

· No decisions have been made that would alter significantly the intended level of service provision for any significant activity undertaken by or on behalf of the Council, or would transfer the ownership or control of a strategic asset to or from the Council.

Next Steps

To continue to improve the safety culture at CHBDC, while implementing the initiatives laid out in the Health and Safety Action Plan for 2020 and 2021, and to work through the actions laid out in the 2019 Gap Analysis Report.

|

RECOMMENDATION That, having considered all matters raised in the report, the report be noted. |

|

31 March 2021 |

6.5 Audit Findings Monitoring Report

File Number:

Author: Brent Chamberlain, Chief Financial Officer

Authoriser: Monique Davidson, Chief Executive

That, having considered all matters raised in the report, the report be noted.

PURPOSE

The purpose of this report is to track and update the committee on audit recommendations from recent audits.

significance and engagement

This report is provided for information purposes only and has been assessed as not significant.

BACKGROUND

Over the course of each year Council undertakes a number of audits that look at the activities of Council’s Corporate Services functions.

This include internal audits which test Councils Policies and Procedures to ensure they are fit for purpose and that they are being adhered to, but also includes external audits of financial reporting to the public (whether this is an Annual Report, or a Long Term Plan). These external audit focus on the quality of data being supplied, and the controls that Council has in place to ensure accuracy of data, controls to ensure protection of public funds, and transparency of information supplied.

Officers will work between the March and May Risk and Assurance Committee meeting to incorporate NZTA Audit Report Recommendations into the report. It is anticipated that this report will become a standing item at every Committee meeting.

DISCUSSION

Below are the findings/recommendations of the last three audits undertaken on the Corporate Services Activities:

Internal Audit: Procurement and Purchasing (undertaken November 2019)

|

Observation |

Recommendation |

Actions Taken |

|

Managing Conflicts of Interest The Council adopted the Procurement and Contract Management Policy in October 2018. The Policy sets the Council’s requirements and expectations in relation to how procurement should be done at the Council. The responsibility for the Policy has been assigned to Group Manager Corporate Support and Services. The Policy requires ‘all staff involved in the preparation and execution of a public procurement process to complete a Conflict of Interest (CoI) declaration which is to be approved by the delegated financial authority for the procurement’. We received a list of current major contracts from the Council’s Contract Register and selected a sample to check how the decision to procure was made, how the supplier was selected, what procurement methods were used in the selection (tender, direct engagement, pre-approved supplier list), whether all documentation (such as conflicts of interest forms) were completed and documented. For our sample of 5 procurements we noted the following: • For 2 procurements the CoI declarations were not prepared at all. • For 2 procurements the CoI declarations were prepared by the members of the evaluation team but were approved by the 3 Waters Programme Manager instead of the appropriate delegated financial authority (the Council for one and the GM for the other). • For 1 procurement (for which the procurement plan was approved on 29/8/19) the CoI hasn’t been done at the time of our review (November 2019), although the Procurement Plan that went for approval to the Council said that the CoI declarations had been approved. Risk If the Council doesn’t effectively manage the conflicts of interest across its procurement activities, it can make inappropriate purchases or enter into inappropriate contracts which could be challenged by other suppliers or ratepayers. Poor management of conflicts of interest also increases risk of corruption. |

The Council should effectively communicate the requirements of its Procurement and Contract Management Policy across relevant staff involved in procurement. This could be achieved through a Council-wide training session or workshop for staff.

|

Officers have worked with the PMO (Project Management Office) to ensure that conflict of interest forms are correctly filled out and kept for all of Councils significant procurements. Officers are in the process of reworking the procurement manual to incorporate the Progressive Procurement Toolkit and Supplier Guide recently developed by Hastings District Council on behalf of the 5 Hawkes Bay Councils. It is envisaged that this work is completed and an all staff training session on the new manual, toolkit, and supplier guide is rolled out by 30 June 2021. |

|

Managing procurement outside the Infrastructure Team As part of our testing, a listing of annualised Council spend by supplier was provided. From this a random sample of suppliers with annualised spends of over $50k were selected for testing. The testing consisted of how the decision to procure was made, how the supplier was selected, what procurement methods were used in the selection (tender, direct engagement, pre-approved supplier list), whether all documentation (such as conflicts of interest forms) were completed and documented. For our sample of 6 vendors with purchases between $25k and $200k we were unable to find: - Procurement Plans - Vendor selection documentation - Conflicts of interest declarations for personnel involved in the procurement activities.

According to the Council’s Policy we would expect that these procurements would either use quotes from preferred or panel suppliers. If existing contracted, preferred or panel suppliers are not appropriate then a Procurement Plan that recommends another approach must be prepared (e.g. an open tender or direct award to a high performing supplier). Risk If the Council doesn’t comply with its Policy, the Council may procure goods or services at a higher price or may spend public money inappropriately. The Council’s decisions can be challenged by ratepayers or suppliers. This may lead to legal or reputational damage. |

Like the point above, the Council should effectively communicate the requirements of its Procurement and Contract Management Policy across relevant staff involved in procurement outside the Infrastructure team. This could be achieved through a Council-wide training session or workshop for staff. |

As above |

|

Procurement Strategy The Policy requires the Council’s ELT team to ‘oversee the development and maintenance of a rolling three year procurement strategy’. At the time of our review no such strategy has been developed. Risk If the Council doesn’t comply with its Policy, the Council may procure goods or services at a higher price or may spend public money inappropriately. The Council’s decisions can be challenged by ratepayers or suppliers. This may lead to legal or reputational damage. |

The Council should develop the three-year procurement strategies are required by the Policy.

|

The current policy no longer requires Procurement Strategies to be developed, as it was determined they were essentially a distraction from individual Procurement Plans developed. |

|

Lack of oversight of procurement activities A large number of instances of non-compliance with the Council’s Policy (findings 1-3 above), requires the Council to monitor the extent to which the business units comply with the requirements of the Policy. This becomes even more important given the decentralised procurement operating model at the Council, i.e. when each business unit performs its own procurements without a centralised support. Currently no monitoring is performed by the Council to ensure all purchases and procurement activities comply with the Policy and there is varying degrees of understanding of procurements activities happening across the Council. In addition, there is limited procurement reporting to the Executive Team and the Council. We understand that reporting is on an exception basis. As a result, this reduces Managements oversight on procurement activities. Procurement reporting would provide an overview of large value, high risk or complex procurements. It would also provide valuable insights into the activities of other departments. Risk The lack of an effective process to monitor compliance with the Council’s Policy increases the risk that the Council’s purchases may not meet the policy requirements and the Council’s expectations. |

The Council should implement a formal process to review the Council’s compliance with the requirements of the Policy. This could be done by regularly reviewing a sample of purchases to check whether all Policy requirements have been met. The results of this ‘audit’ should be communicated to the ELT. The responsibility for this work should either sit with the Group Manager Corporate Support and Services (as the Policy Owner) or could be delegated to the 3 Waters Programme Manager (as a ‘Centre of Procurement Excellence’ within the Council). |

Council’s finance team has recently had a small restructure which has introduced procurement as an element into the job description of a staff member other than the Chief Financial Officer. The intention is that this person gets trained in procurement, and they act a procurement advisor to staff undertaking procurement, and that this person commences quarterly checks of adherence to policy. This training has commenced. |

|

Lack of additional guidance to assist employees in the procurement process The Council has started drafting a Procurement Manual to provide additional guidance and support to the Council’s personnel involved in procurement activities. However, at the time of our review, this work hasn’t been finished yet. The Council’s 3 Waters team has developed several templates (e.g. Procurement Plan) to assist with its major procurements, however they do not cover the end-to-end procurement process and additional templates need to be created (e.g. probity checklists, RFx templates, supplier recommendation templates, etc.). In a de-centralised environment, we would expect a suite of tools and templates such as procurement plans, tender documents and checklists to guide employees. Risk The absence of additional guidance material to assist staff during procurement may lead to a situation where staff do not comply with the Council’s procurement process. |

Finalise the Council’s Procurement Manual and communicate it to all personnel involved in procurement. Develop additional tools and templates to assist employees in the procurement process. The need for these templates will be identified in the Manual. The Manual and templates should be developed or reviewed by procurement and or legal professionals. |

Council adopted a rewritten procurement policy in 2020. Officers are in the process of reworking the procurement manual to incorporate the Progressive Procurement Toolkit and Supplier Guide recently developed by Hastings District Council on behalf of the 5 Hawkes Bay Councils. It is envisaged that this work is completed and an all staff training session on the new manual, toolkit, and supplier guide is rolled out by 30 June 2021. |

|

Incorrect system-enforced authorisation limits The authorisation limits in the Council’s core system, MagiQ, are not in line with the limits established in the Council’s Delegations Register. As a result, staff members are able to approve purchases above the levels of authority they have been granted. We noted the following exceptions: Brent Chamberlain Bridget Gibson Craig Ireson Graham Manning Ian Cover |

Review the authorisation limits in MagiQ and ensure they are in line with the current Delegations Policy. If it is identified that for practical reasons, higher limits may be required for approving payments then a review of the delegated authorities should be undertaken. The Council can also perform a data analytics test to understand whether these incorrect delegations settings have actually resulted in any incorrectly authorised purchases. |

The limits in Magiq were corrected following this audit, and then were tested again as part of the Ernst Young Year End Audit in August/September 2020. |

|

Policies are not up to date Procurement and Contract Management Policy The Council’s Procurement and Contract Management Policy was due to be reviewed on 31 October 2019. At the time of our work in November 2019 the Policy still hasn’t been reviewed. This was largely due to a change in the Group Manager Corporate Support and Services. Credit Card Operation Procedure The Council has a Credit Card Operation Procedure which defines the Council’s use of credit cards. The Procedure specifies that there should only be one card and it should be operated by the Chief Executive. We understand that the Council uses two cards: one used by the Mayor and the CE; one used by the Group Manager Corporate Support and Services for staff travel expenses and other minor purchases. |

Ensure the Procurement and Contract Management Policy is up to date. Review the Credit Card Operation Procedure to ensure it reflects the current Council’s practice of using the credit cards. |

Policies have been updated: Procurement Policy 18/9/2020 Credit Card Operation 2/6/2020 |

External Audit: Year End (Undertaken August/September 2020)

|

Observation |

Recommendation |

Actions Taken |

|

Process documentation and reliance on key individuals There are certain roles within the Council that require specialised knowledge in order for the role to be performed efficiently and effectively. An example of this is the maintenance of the data for the three waters infrastructure assets and the associated valuation of these assets where knowledge of relevant systems plus the underlying subject matter is required. We observed that there was a reliance on the person filling this role and there were limited other staff members that were able to assist with key audit procedures relating to the valuation of the three waters infrastructure assets and how the valuation linked to the underlying data. There was also a lack of supporting documentation for the valuation exercise completed and the documentation that was available didn’t contain sufficient detail. |

We recommend that CHBDC broaden the number of staff that have a working understanding of the processes and controls relating to infrastructure assets and in particular data management and valuation processes for the three waters assets. We also recommend processes notes be retained by CHBDC to ensure that in the absence of key individuals, processes can continue to be performed and there is clarity with respect to processes followed historically. |

This is the nature of being a smaller Council where not every position has a clear backup. It did highlight that all key person positions keep good hand over notes as part of role handover on exit. |

|

Compliance with Policies We noted that the CHBDC Treasury Management Policy was not been followed in relation to concentration risk for investments. The Council’s Treasury Management Policy restricts the amount that can be invested with any one counter party to $8m. At 30 June 2020, Council had term deposits with BNZ of $9m. |

We recommend that policies be followed to ensure risk is being managed in a way that has been agreed with those that approved the policy. |

Policy updated on 18/9/2020 to increase this limit to $10m. Currently the maximum investment with any one bank is $7.5m. |

|

Timely update of authorised signatories During our testing of the authorised signatories for online banking, we noted that two employees who left the Council during the year were still listed as authorised signatories. We acknowledge that subsequent to our finding the list of authorised signatories was correctly updated. |

We recommend that banking signatories and approvers be updated on a timely basis. There should also be a process for staff leaving Council to ensure access to IT systems is removed, they are removed as authorised signatories and Council property in returned. This process should be systematically worked through for each employee that leaves Council. |

The paper banking mandates had been updated at the time of audit, but ANZDirect user logins did not reflect the change. This was subsequently corrected before the audit was completed. |

|

Timely closure of credit cards As part of our testing, we identified that there was an active credit card in the name of a former employee. We did additional analysis over the expenses incurred on the credit card to assess what expenses had been incurred on the card since the employee left and noted that all costs were automatic payments for subscriptions that were used by Council. Subsequent to year end, we are aware that the credit card has been cancelled. |

We recommend that management cancel credit cards in a timely manner when individuals leave council. |

The card had been cut up at the time of audit, but due to a number of annual subscriptions coming out of this card, the card wasn’t immediately cancelled. The card was formally cancelled before the audit was complete. |

|

Approval of Expenditure Under the current sensitive expenditure policy, an approver or expenditure cannot benefit personally from the expenditure being claimed. However, through our testing we identified instances where expenditure was approved by a member of staff that benefited from the expense being incurred as well as the approver being more junior that than the individual incurring the expense. |

We recommend that Council update their policy to include a requirement for a “one up” approval of the individual incurring the expenses, this would be a council member in the case of the Mayor’s expenses. |

This item is a carry forward from 2019. Sensitive Expenditure was again retested in 2020 with one breach identified so it remains an audit point. |

|

Land Title Discrepancies We obtained and reviewed the land titles for land owned by the Council on a sample basis to verify the information used by QV in their 2017 valuation of the Council’s land and to validate the land is freehold. We identified several discrepancies between the Council records and the information used by QV. For one title the land information on the title was less than the area valued in by QV. In addition, a number of titles were not able to be obtained. There is a risk the Council records do not contain the most up to date information in relation to land titles. In addition, there is a risk QV may be performing their valuation on incomplete / inaccurate information. |

We recommend a formal review be completed for land held by the council to ensure all land titles are available and the title area reflects the Council’s records and that used by QV. |

This item is a carry forward from 2019. 5 Titles were identified as belonging to CHBDC but had discrepancies with the LINZ records. 3 have now been resolved, and 2 remain: 1092050900 232 Pourerere Beach 1095013300 Hatuma Road

Both these are recorded by LINZ as public reserves with Department of Conservation Ownership |

|

Policies due for update We noted a number of policies are past their date for revision. There is a risk that outdated policies may not reflect the most up to date intentions of Council. It is important policies are updated in a timely manner, particularly when there is public visibility to policies via the council’s website. |

We recommend the Council update the policies, and in the future establish a process to ensure they are updated in a timely manner. |

This item is a carry forward from 2019. Officers are working through a review process to ensure all policies are up to date and significant progress was made during 2020. A paper outlining current status of policies and determining role for Risk and Assurance Committee is planned for May 2021. |

External Audit: Long Term Plan (Undertaken December 2020 – January 2021)

|

Observation |

Recommendation |

Actions Taken |

|

Quality of asset information CHBDC could improve the quality of the information reflected in the Infrastructure Strategy through using a more granular five tier scale to assess data quality and through presenting asset performance information for water supply and waste water. The identification of specific critical assets would also be beneficial. |

|

The understanding of our infrastructure assets is improving and being better documented over time. Officer’s intention is that this is an area of continuous improvement. |

|

Targets for performance measures Some performance measures have targets set at a level notably below current delivery. We would expect targets to usually show continued performance at the current level or provide a degree of challenge for services to improve going forward. |

|

After being challenged by Ernst Young many LOS targets were adjusted. But with many of our mature services with high levels of satisfaction it is not always practical or cost effective to strive for further improvements. Further discussion on this will continue before the close out of the Long Term Plan 2021 – 2031 audit. |

|

Articulation of long term view Council have provided a transparent plan of what is required in the short to medium term due to previous underinvestment in infrastructure assets. Funding this investment results in increased debt and expenditure exceeding revenue for most years of the long-term plan. Going forward Council will need to engage with the community on both when the budget will be able to be balanced and specifically how renewals work will be funded in a more sustainable way. |

|

It is officer’s intent to provide advice to Council in order to strive towards the goal of achieving a balanced budget and they intend reviewing the life expectancy of assets, and therefore depreciation, as more asset conditioning work is undertaken. |

Implications ASSESSMENT

This report confirms that the matter concerned has no particular implications and has been dealt with in accordance with the Local Government Act 2002. Specifically:

· Council staff have delegated authority for any decisions made;

· Council staff have identified and assessed all reasonably practicable options for addressing the matter and considered the views and preferences of any interested or affected persons (including Māori), in proportion to the significance of the matter;

· Any decisions made will help meet the current and future needs of communities for good-quality local infrastructure, local public services, and performance of regulatory functions in a way that is most cost-effective for households and businesses;

· Unless stated above, any decisions made can be addressed through current funding under the Long-Term Plan and Annual Plan;

· Any decisions made are consistent with the Council's plans and policies; and

· No decisions have been made that would alter significantly the intended level of service provision for any significant activity undertaken by or on behalf of the Council, or would transfer the ownership or control of a strategic asset to or from the Council.

Next Steps

Officers will continue to work towards resolution for the audit recommendations listed above that have yet to be resolved. Officers will continue to report any items above until resolution is achieved.

|

RECOMMENDATION That, having considered all matters raised in the report, the report be noted.

|

|

31 March 2021 |

6.6 Review of Elected Member Remuneration and Expenses Policy

File Number:

Author: Brent Chamberlain, Chief Financial Officer

Authoriser: Monique Davidson, Chief Executive

Attachments: 1. Elected Member Remuneration and Expenses Policy ⇩

PURPOSE

The matter for consideration by the Council is the adoption of the updated Elected Member Remuneration and Expenses Policy

RECOMMENDATION for consideration

That having considered all matters raised in the report:

a) That the report be received.

b) That the Committee endorse and recommend to Council they adopt the proposed amendments to the Elected Member Remuneration and Expenses Policy” to include additional paragraphs on Receipt of Gifts.

BACKGROUND

At the 12th November 2020 Risk and Assurance Meeting, a paper entitled Review of Sensitive Expenditure Policy was tabled. This paper reviewed both the Sensitive Expenditure Policy and the Elected Member Remuneration and Expenses Policy. One of the resolutions of this meeting was that the Elected Member Remuneration and Expenses Policy should be expanded to include further clarity about the procedure upon “receipt of gifts”.

DISCUSSION

Currently the Sensitive Expenditure Policy (which only applies to staff and Council contractors) sets out the procedures for staff/contractors who receive gifts, and the establishment of a gift register, however the Elected Member Remuneration and Expenses Policy was largely silent on this matter.

When this policy was reviewed on the 12th November 2020 Risk and Assurance Meeting it was requested that this area of the policy be bolstered to be more reflective of the staff version, and an Elected Member Gift Register be established.

Currently the policy states:

“The receiving of a gift is not strictly ‘sensitive expenditure’; nevertheless, it is a sensitive issue. It is especially important that receiving a gift does not alter Councils decision-making, as this could be perceived as acting without impartiality or integrity.

Under no circumstances should a gift be accepted from an organisation or individual who is involved in the process of negotiating or tendering for the supply of goods or services to the Council.”

What is proposed is that the following additional paragraphs be added to the existing policy:

“If a gift is accepted the Mayor and Governance Support Officer must be notified, and the Mayor shall consider the following points to determine the appropriate disposal of any gift, reward, discounts or inducements:

a) All gifts received by Councillors are to be recorded in the Gift Register.

b) The Mayor may then distribute any such gifts including;

· Allowing the recipient to keep the gift.

· Consideration will be given to equity, and the association with provider and appropriateness of the person receiving the gift.

c) Councillors may retain the gift when they are small business courtesies such as pens, diaries, calendars, caps and t-shirts, all of which are to be recorded on the Gift Register.”

This would bring alignment with the Staff and the Elected Member policies in this area.

RISK ASSESSMENT and mitigation

This policies key outcome is to uphold the reputation and integrity of Council, and to ensure that Council’s use of public funds is open and transparent.

FOUR WELLBEINGS

This policy is about ensuring that Council is fiscally prudent with Council’s resources.

Delegations or authority

This policy is being brought to the Risk and Audit Committee as part of an agreed work program and is one method that Council uses to mitigate the risk of perception of misuse of public funds.

sIGNIFICANCE AND ENGAGEMENT

In accordance with the Council's Significance and Engagement Policy, this matter has been assessed as of minor significance.

OPTIONS Analysis

Officers are recommending that the “Elected Member Remuneration and Expenses Policy” be expanded to include additional paragraphs on receipt of gifts.

Risk and Audit has the ability to endorse the proposed change and recommend to Council that the policy be amended:

1. Accept Officers recommendation that the “Elected Member Remuneration and Expenses Policy” be expanded to include the additional paragraphs on receipt of gifts, and this change is recommended to Council for adoption.

2. Reject Officers recommendation that the “Elected Member Remuneration and Expenses Policy” be expanded the additional paragraphs on receipt of gifts.

Recommended Option

This report recommends option one, that the “Elected Member Remuneration and Expenses Policy” be expanded to include the additional paragraphs on receipt of gifts, and this change is recommended to Council for adoption, for addressing the matter.

NEXT STEPS

Assuming the recommendations above are adopted, officers will update the “Elected Member Remuneration and Expenses Policy” as proposed.

|

RECOMMENDATION That having considered all matters raised in the report: a) That the report be received. b) That the Committee endorse and recommend to Council they adopt the proposed amendments to the Elected Member Remuneration and Expenses Policy” to include additional paragraphs on Receipt of Gifts. |

|

31 March 2021 |

6.7 Treasury Management Monitoring Report

File Number: COU1-1408

Author: Brent Chamberlain, Chief Financial Officer

Authoriser: Monique Davidson, Chief Executive

Attachments: Nil

That, having considered all matters raised in the report, the report be noted.

PURPOSE

The purpose of this report is to provide an update on Treasury Management and Policy Compliance.

significance and engagement

This report is provided for information purposes only and has been assessed as not significant.

BACKGROUND

Council is required under the Local Government Act 2002 to have 3 policies:

· Treasury Management Policy

· Liability Management Policy, and

· Investment Policy

The rationale for the policies is to ensure prudent use of public funds, manage investment returns, borrowing costs, and to minimise the risk of loss of public funds.

In practice Central Hawkes Bay District Council has combined them into a single policy covering all 3 topics.

Council’s current policy was adopted in May 2016.

In October 2020 Officers and Council have reviewed this policy, with the view to consult on the proposed changes with the public as part of the Long Term Plan Consultation Document.

DISCUSSION

Investments

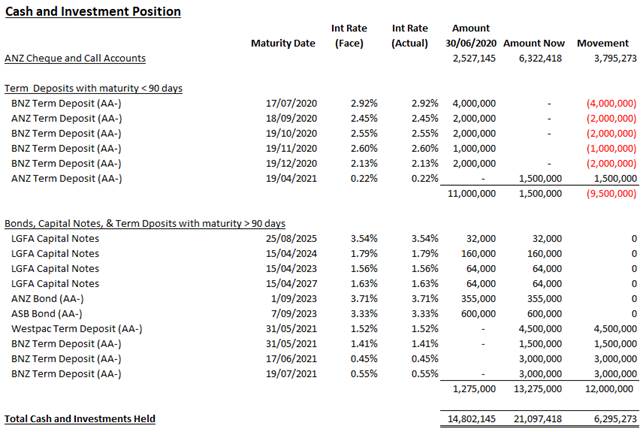

At the 28th February 2021, Council was holding $6.3m in funds on call (up $3.8m from 30 June 2020). Much of this is due to the timing of quarterly rates receipts, and the first $5.5m of the 3 Waters Reform monies having been received.

In addition Council was holding $13.5m in term deposits ($11m as at 30 June 2020) spread across 4 maturities and 3 different banks, $320k in capital notes ($320k as at 30 June 2020), and $955k ($955k as at 30 June 2020) in bank bonds.

These investments are listed below:

During the last six months investment returns have fallen further, with the most recent term deposits only achieving returns of 0.5% compared to 2.5% nine months earlier.

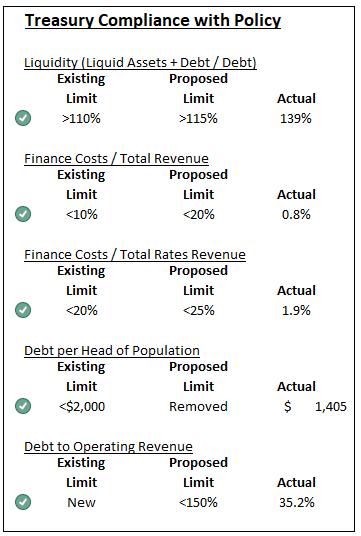

Council’s maximum exposure with any one bank is only $7.5m which is compliant with Council’s policy ($8m limit) and the quality of the investments (credit worthiness) is also compliant with policy.

Borrowing

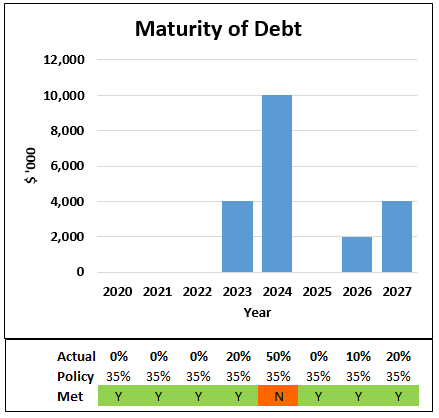

At the 28th February 2021 Council had $20m of external debt drawn ($20m 30 June 2020).

Council become a guarantor for LGFA (Local Government Funding Authority) on the 10th February 2021 which will then allow Council to borrow further funds (LGFA limit 175% of its operating revenue, proposed limit 150%, currently Council is at 35% to total income, or 59% if you exclude one-off PGF and 3 Waters funding).

On the following page are a list of Council’s debt ratios as per the existing policy and the proposed policy:

As at 28th February 2021, Council is holding sufficient funds to meet its financial obligations (liquidity ratio), it is within its debt ceiling (debt per head of population and debt to operating revenue ratios), and it is within its financial costs ratios.

Councils proposed policy states that “no more than the greater of $10m, or 35% of Council’s total debt can mature in any 12 month rolling period”. As at 28th February 2021 the only 12 month period that exceeds 35% of all debt maturing in a 12 month period is 2024 where $10m matures, which is still inside the proposed policy.

The table below shows the details of Council’s current debt portfolio:

Implications ASSESSMENT

This report confirms that the matter concerned has no particular implications and has been dealt with in accordance with the Local Government Act 2002. Specifically:

· Council staff have delegated authority for any decisions made;

· Any decisions made will help meet the current and future needs of communities for good-quality local infrastructure, local public services, and performance of regulatory functions in a way that is most cost-effective for households and businesses;

· Any decisions made are consistent with the Council's plans and policies; and

· No decisions have been made that would alter significantly the intended level of service provision for any significant activity undertaken by or on behalf of the Council, or would transfer the ownership or control of a strategic asset to or from the Council.

Next Steps

Officers will continue to provide quarterly updates on Treasury Management.

|

RECOMMENDATION That, having considered all matters raised in the report, the report be noted. |

|

31 March 2021 |

6.8 Long Term Plan 2021-2031 Risk Mitigation

File Number:

Author: Brent Chamberlain, Chief Financial Officer

Authoriser: Monique Davidson, Chief Executive

That, having considered all matters raised in the report, the report be noted.

PURPOSE

This report is presented to the Risk and Assurance Committee to consider the risks associated with the Long Term Plan 2021-2031, and associated budget and policy position of Council.

significance and engagement

This report is provided for information purposes only and has been assessed as not significant.

BACKGROUND

The process to develop the Long Term Plan 2021-2031 began in May 2020. Following this was a detailed and robust LTP pre-engagement process through June and July 2020 as part of our ‘Thriving Future’.

Development of the Long Term Plan has progressed through numerous Council Workshops, Committee and Council meetings, and while formally beginning in May 2020, many of the building blocks have been developed over the last three years since the adoption of the 2018 – 2028 Long Term Plan.

The Long Term Plan consultation document, and the proposed budgets it contains, has been through an external audit by Ernst Young and is now out for public consultation.

Communication of this consultation, and the consultation of itself has taken various forms including website advertising, Facebook advertising, newspaper advertising, radio advertising, town hall meetings and special interest group meetings.

The consultation document and the supporting document can be found here:

https://chbdc.mysocialpinpoint.com.au/facingthefacts

DISCUSSION

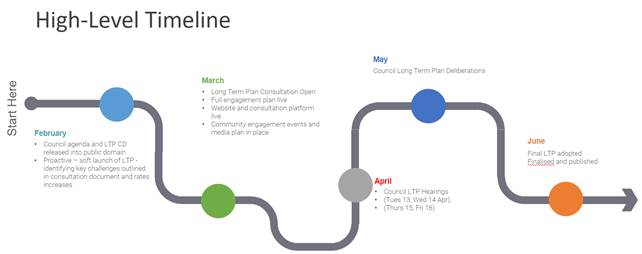

At the previous Risk and Assurance Committee meeting the LTP was discussed and the question of “risk” was raised and Officers were asked to report back on what the risks are in this process.

As the adoption of LTP has a significant impact on the public for the next 10 years, it must be audited and publicly consulted on (both through public meetings and LTP Hearings).

At the time of writing we are half way through the public consultation process. The timeline from here looks like this:

Public consultation includes, but isn’t limited to:

|

Face to face |

Media |

Social |

Print collateral |

Direct Mail |

|

Site tours Landfill tours – FB Live + Video Three waters tours – FB Live + Video |

CHB Mail Double page spread with survey first week of consultation Adverts throughout consultation

KIC x4 weeks

Editorial (through press release / interview with CHB Mail) |

Facebook and Insta campaign posts prompting discussion Challenges 1, 2, 3, 4 Financial Strategy Infrastructure Strategy Bylaws |

Consultation Document Council office Libraries Website |

Rates letter + flyer NZ Post 1 March Email |

|

Town Halls Tikokino Porangahau Waipawa Takapau Ongaonga Online through social pinpoint |

Radio – Central FM Radio interviews (Mayor’s Wed session)

Radio ads |

Facebook lives – hosted by mayor / councillors with staff –on site showcasing services in action / repairs |

Flyer – summary (A3 folded) Tours Libaries Waipawa pool Community venues Reception |

Existing stakeholder newsletters |

|

Community Meetings Rotary Grey Power Probus Youth group / council Positive Ageing View point |

Media releases With Council agenda Following Council meeting Feb Launch of consultation Mid-consultation End of consultation Deliberations and final plan |

Insta / Facebook stories Sharing content from the councillor visits on location through facebook live session ASMR posts on instagram |

Councillor Packs - - marketing collateral - presentations |

|

|

Cuppa with a councillor |

|

Tik Tok – CHB – The LTP Challenge |

Posters Libary Waipawa pool Community venues Reception |

|

|

School visits Councillors visit their local schools |

|

|

Display boards for tours - Waste and recycling - Three waters |

|

Obviously when you build a budget (particularly a 10-year view) it is based on a number of assumptions (which all come with risk that they don’t work out). The assumptions contained in the LTP include, but aren’t limited to:

|

Forecasting Assumption |

Risk |

Likelihood of Occurrence |

Financial impact |

Risk Mitigation Factors |

||||||||||||||||||||||||||||||||||||

|